{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

2727 Xanthia Court, Denver, CO 80238, +1-720-453-8045 (phone)

E-mail: info@gscassociates.com

Table of contents

This document is a tutorial on the types of information found in tax lists and how that information can be used in historical and genealogical research. The emphasis is on the early tax lists of Bedford County, Tennessee but most of the information applies to the tax lists of other locations as well. The information contained in each tax list along with some general principles explaining the meaning of some of that information is described in the following sub-clauses.

Tax lists enumerate property under the name of the person responsible for paying the tax. This is most often the owner of the property, however a person who rented or leased the property may be listed instead of the owner in some cases. Also a person who actually resides in a different location will be listed in the tax list of a civil district if their property (usually land or slaves) is located in that district.

Free male persons of certain ages who owned no taxable property still had to pay a tax called a "poll tax". In the early tax lists of Bedford County, Tennessee all free males who resided in a given civil district and whose age was at least 21 but less than 50 had to pay a poll tax in that district. Females who were the heads of households are also listed.

The property taxed in each year that tax was collected was determined by an act of the Legislature of Tennessee that established the collection of the tax in that year. Not all types of property were taxed in each year, so the lists for each year may provide slightly different information.

Tax lists often contain counts of "white polls" and "black polls". The word "poll" used in this manner means "a counting of heads or people; a census" and does directly relate to any tax paid for the purposes of voting. In early Bedford County, Tennessee tax lists the abbreviation "WP" is used for "white poll" while slaves are listed as "slaves" and not "black polls".

When lands were given out by grant in early Tennessee and North Carolina, a portion of each section was set aside "for the use of schools". These large tracts of land were not needed immediately for school purposes so much of the land was leased for agriculture. Leased school land was taxed at a different rate from private land and is listed separately on tax lists.

Lots in an established town were listed separately and taxed at a different rate from land used for other purposes. Some early Bedford County, Tennessee tax lists include "town lots" as a taxable item.

Example from the 1812 tax list

The 1812 tax list contains the following information for each entry:

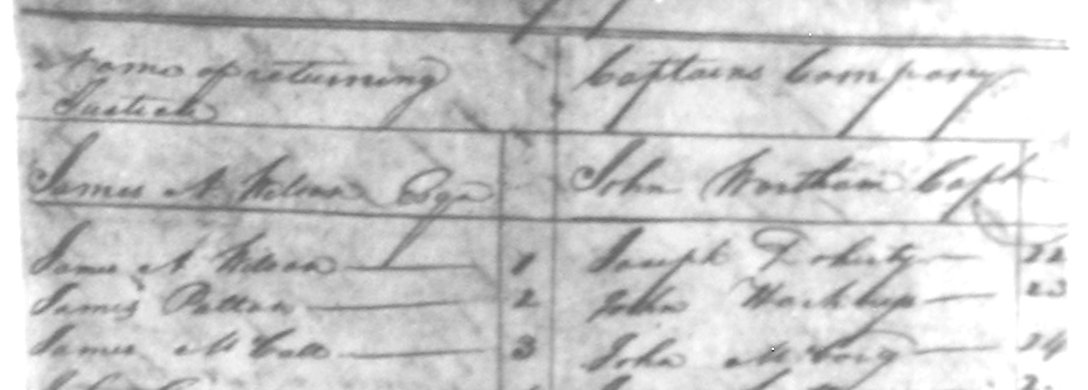

Example: James Patton, 1

Example 1

(left half page) from the 1814 tax list

Example 2 (right half page) from

the 1814 tax list

The prose at the front of the list says:

"General list of lands, lots of ground and their improvement dwelling houses and slaves within the 5th assessment district composed of Bedford County within the State of Tennessee owned or possessed or under the care and management of persons on the 1st day of February 1814 residing within the same."

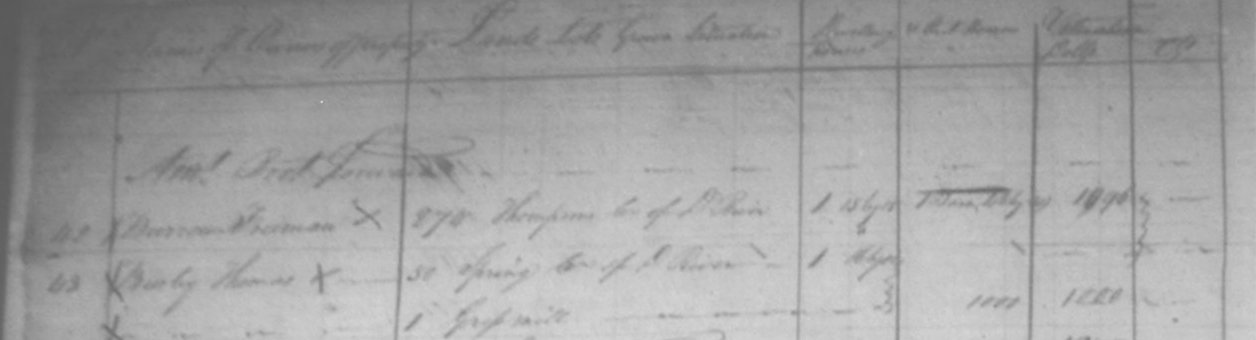

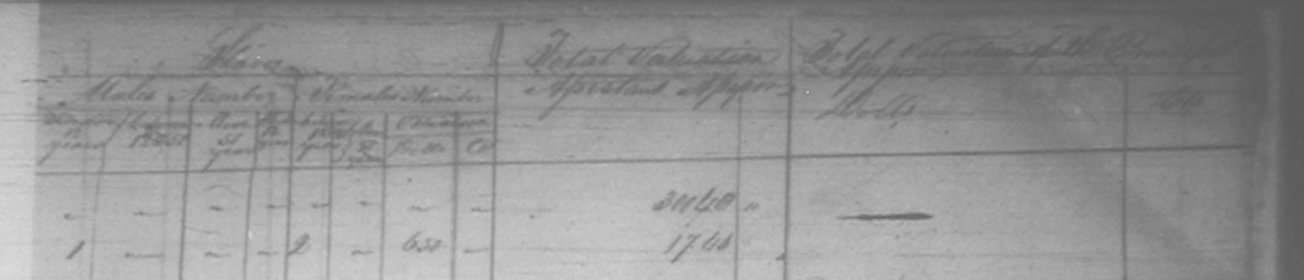

The 1814 tax list contains the following information for each entry:

Example: Christopher Shaw, 450 acres in Garrison Fork, Puncheon Camp Creek, no dwelling houses, 4 out buildings, valuation $3030.50, 1 Male Slave under 12 years, 6 Male Slaves between 12 and 51 years, 0 Male Slaves over 51 years, 2 Female Slaves under 12 years, 3 Female Slaves between 12 and 51 years, 1 Female Slave over 51 years, valuation of slaves $4,150

Example from the 1836 tax list

The 1836 tax list contains the following information for each entry:

Example: Nobel J. Majors, 62 acres, $320 value, $0.32 tax, 86 acres of school land, $4.30 value, $0.43 tax, no carriages, no slaves, 1 white poll, $0.25 tax, $.50 State tax, $1.00 total tax

Example from the 1837 tax list

The 1837 tax list contains the following information for each entry:

Example: Jacob Coffman, 36 acres, $275 value, $0.13 1/2 tax, 10 acres of school land, $25 value, $0.01 tax, no town lots, no slaves, 1 white poll, $0.13 tax, $0.12 state tax. $0.25 total; tax

Example from the 1838 tax list

The 1838 tax list contains the following information for each entry:

Example: William Eoff, 355 acres, $2,800 value, <blank> tax, 200 acres school land, $1,600 value, $0.76 tax, no town lots, 3 slaves, $1,500 value, >blank> tax, 1 white poll, <blank> tax, $2.15 state tax, $6.84 total tax

Example from the 1839 tax list

The 1839 tax list contains the following information for each entry:

Example: Thomas B. Jeffries, 175 acres, $800 value, $0.40 tax, 25 acres school land, $300 value, $0.10 tax, no town lots, 3 slaves, $1,700 value, $0.85 tax, $0.12 tax, <blank> state tax, $1.07 total tax

The US census prior to 1850 did not list the names of children. It also gave only approximate ages for each individual in a household - often only within a category spanning ten years, such as age 20 to 30. Early tax lists are extremely valuable because examining lists over a range of years can show with an accuracy of one year when a tax payer turns certain ages, most often age 21 or age 50. Further, males coming of age and paying tax for the first time are almost always listed immediately after their father (or mother) in the tax list. Unfortunately, so few early lists for Bedford County, Tennessee survived that this is not as valuable a technique as in other locations.

Example 1: The following example from Montgomery County, Virginia tax lists shows four sons of Samuel Reidinger (John, Stephen, George, and Michael Reidinger) coming of reportable age (16 in Virginia at that time) and then later appearing in the tax lists besides their father as they turned 21 and became of taxable age.

The categories in these lists (except where notes) are:

1816 Cyrus Robinson's District:

Samuel Ridinger 2-0-2-0... $0.36

John Ridinger 1-0-2-0... $0.36

1817 William Currin's District:

Samuel Ridinger 3-0-2-0... $0.36

John Ridinger 1-0-2-0... $0.36

1818 William Currin's District:

Samuel Redinger 2-0-1-0... $0.18

John Redinger 1-0-1-0... $0.18

Stephen Redinger 1-0-0-0... $0.00

1819 William Currin's District:

(beginning this year the category "Slaves" was divided into two

categories: Slaves between 9 and 12 years old and Slaves above 12 years old)

John Ridinger 1-0-0-1-0... $0.18

Stephen Ridinger 1-0-0-0-0... $0.00

George Ridinger 1-0-0-1-0... $0.18

<Samuel Ridinger not listed this year>

1820 William Currin's District:

Samuel Rindinger 1-0-0-1-0... $0.18

John Ridinger 1-0-0-2-0... $0.35

Stephen Ridinger 1-0-0-0-0... $0.00

George Ridinger 1-0-0-1-0... $0.18

1821 William Currin's District:

Samuel Rindinger 1-0-0-1-0... $0.13 1/2

John Ridinger 1-0-0-2-0... $0.27

Stephen Ridinger 1-0-0-0-0... $0.00

George Ridinger 1-0-0-1-0... $0.13 1/2

Michael Ridinger 1-0-0-0-0... $0.00

Example 2: Tax lists typically say when an individual responsible for paying tax is acting in some court-appointed capacity.

1837 Tax List, Bedford County, Tennessee, 1st CD, Mary Shaw, guardian for R. Shaw: 150 acres, $1,500 value, $0.75 tax, 90 acres school land, $450 value, $0.22 1/2 tax, no town lots, 6 slaves, $3,100 value, $1.55 tax, no white polls, $2.30 state tax, $5.05 total tax

Example 3: A person residing out of district may have another person designated as his "agent" for purposes of paying local taxes. Often there is some relationship between the individuals in such a case:

1836 Tax List, Bedford County, Tennessee, 5th CD, McKinzie by William Head, agent: 833 1/2 acres, $4,000 value, $4.00 tax, no school land, no town lots, no slaves, no white polls, $2.00 state tax, $4.00 total tax

Example 4: Sometimes there are several individuals with similar or the same names in a tax list. In this case the list makers sometimes made additional annotations following the individual's name, often stating the relationship to some other individual.

Example 5: The following tax list data shows George Usselton (who was born on 10 Aug 1762 in Shrewsbury Parish, Kent, Maryland) turning age 50 and no longer having to pay tax:

Tax List, Rutherford County,Tennessee 1812, page 80 George Usselton No land owned 1 free poll 3 black polls total tax: $1.31 1/2

Tax List, Rutherford County,Tennessee 1813, page 64 George Uselton 80 acres no free polls 2 black polls total tax: $0.90 3/8

Tax lists can usually show within a year when a family moves to and/or leaves a location. The following example from the tax lists of Montgomery County, Virginia shows the Samuel Reidinger family arriving in Montgomery County in 1800 or 1801 and then moving on to Warren County (and later Bedford and Coffee counties, Tennessee, in 1822 or 1823. It also shows associated families that moved from York County, Pennsylvania to Montgomery County, Virginia at about the same time:

Example:

1796:

No Reidingers

1797:

No Reidingers

1799:

No Reidingers

1800:

No Reidingers

Moricle (Christopher, George) first appears

Miller (Adam, Phillip, William, Peter) first appears

1801 James Barnett's District (list submitted 15 August 1801):

Categories: Blacks above 12, Horses, Ordinary licenses, Carriages with two wheels, No. Stud Horses, Rates for Season (single rate), and Amount of Tax in dollars and cents

Samuel Ritinger 0-3-0-0

$0.36

Also listed this year: Jacob and Christian Epperly, John, William and Jacob Morricle, Daniel Spangler. George and Jacob Sowers and Daniel Shelor, Nathaniel Wickham

[1802 - 1820 omitted in this example]

1821 William Currin's District:

Samuel Rindinger 1-0-0-1-0... $0.13 1/2

John Ridinger 1-0-0-2-0... $0.27

Stephen Ridinger 1-0-0-0-0... $0.00

George Ridinger 1-0-0-1-0... $0.13 1/2

Michael Ridinger 1-0-0-0-0... $0.00

1822 William Currin's District:

The 1822 list is missing the last pages, from "N" and following.

1823 William Currin's District:

George Ridinger 1-0-1-0... $0.12

1824 William Currin's District:

George Ridinger 0-3-0... $0.36

By analyzing the property that a person pays taxes on you can determine:

Example: All of the other examples in this tutorial give lists of the taxable property owned by individuals.

Tax lists will often list property belonging to the heirs of an estate during the period that the estate is in probate under either the name of the executor or administrator or simply in a form like "Heirs of John Doe" or "John Doe heirs". By observing changes in listings over several years, a date of death can be approximated and sometimes even the heirs determined.

Example 1: 1837 Tax List, Bedford County, Tennessee, 1st CD, John Gregory heirs: 61 3/4 acres, $617 value, $0.31 3/4 tax, no school land, no town lots, 2 slaves, $1,600 value, $0.50 tax, no white polls, $1.10 1/2 state tax, $2.21 3/4 total tax

Example 2: 1836 Tax List, Bedford County, Tennessee, 4th CD, R. H. Majors for Clardy's heirs: 200 acres, $1,600 value, $1.60 tax, no school land, no town lots, 2 slaves, $900 value, $0.90 tax, no white polls, $1.25 state tax, $2.50 total tax

1837 Tax List, Bedford County, Tennessee, 4th CD, Robert H. Majors, Executor for R. Clardy's heirs: 200 acres, $1,600 value, $1.60 tax, no school land, no town lots, 1 slaves, $500 value, $0.25 tax, no white polls, $1.15 state tax, $2.30 total tax

Example 3: This example shows Joseph A. Arnold and two likely sons listed on adjacent lines in the tax list. In the next year, Joseph A. Arnold is probably deceased because his listing says "Joseph A. Arnold, Administrator":

1836 Tax List, Bedford County, Tennessee, 10th CD, Joseph A. Arnold: 150 acres,... with John W. Arnold, 50 acres,... and Elisha Arnold 48 acres,... listed on the next two lines

1837 Tax List, Bedford County, Tennessee, 10th CD, Joseph A. Arnold, Administrator: 150 acres,... with John W. Arnold, 50 acres,... and Elisha Arnold 48 acres,... listed on the next two lines

Property that passes to an individual through probate was not generally conveyed by recorded deeds. By looking for a set of increases in land owned by several individuals in a single year, property divisions recorded in lost probate records may be identified. This applies to both land and slaves. Also, the disappearance of a male landowner from the tax list and his replacement by a female with the same surname and amount of land discloses the given name of a spouse that would not have been recorded in early census data.

In many counties (but not Bedford County, Tennessee) tax lists itemized all newly purchased or inherited property for that tax year. This information can be correlated with that in other records, such as deed books and probate or county court records.

Example 1: In Bedford County, Tennessee in 1837 the tax list itemized in a special list all of the names and property that moved into the 11th CD of Bedford County when Marshall County, Tennessee was established and most of the 12th through 17th CDs of Bedford County became parts of Marshall County, Tennessee.

Even without an explicit list of newly acquired property, changes in the amount of taxable property between tax years indicates purchase, inheritance, sale, or sometimes lease of property.

Here is a partial transcription of the 1814 tax list of Bedford County, Tennessee. This provides a good idea of the sort of information found in this list.

Copies of the seven earliest surviving tax lists of Bedford County, Tennessee (1812, 1814, 1836, 1837, 1838, and 1839) are available on CD-ROM from GSC Associates. Click here to learn more.

Copyright 2003 GSC Associates. All rights reserved

| GSC Associates 2727 Xanthia Court, Denver, CO 80238, +1-720-453-8045 (phone) E-mail: info@gscassociates.com |